Silver Doctors

Silver Doctors

Economy

Reverse Repos Go Parabolic: ‘Liquidity Shock’ Derivatives Melt-Down Has Begun!

by Dave Kranzler, Investment Research Dynamics, via Silver Doctors.com:

A reverse repurchase agreement, also called a “reverse repo” or “RRP,” is an open market operation in which the Desk sells a security to an eligible RRP counterparty with an agreement to repurchase that same security at a specified price at a specific time in the future. LINK…IMF tells regulators to brace for global ‘liquidity shock’ –LINK.

The financial news spin-doctors are attributing today’s abrupt sell-off to a report of a Bloomberg terminal outage and to a report that China has expanded its list of stocks available for shorting. This explanation for the plunge in stocks globally is so absurd it almost leaves me speechless.

I have been postulating since mid-December that the strange volatility we’ve been experiencing in the markets – combined with the most intensive effort I’ve ever seen by the Plunge Protection Team (the Fed + the Treasury’s Working Group on Financial Markets) to prop up the stock market and keep a manipulative cap on gold – is occurring because there’s is a massive derivatives melt-down going on behind the scenes. The volatility reflects the turmoil and the market intervention in stocks and precious metals reflects the effort to keep the problem covered up.

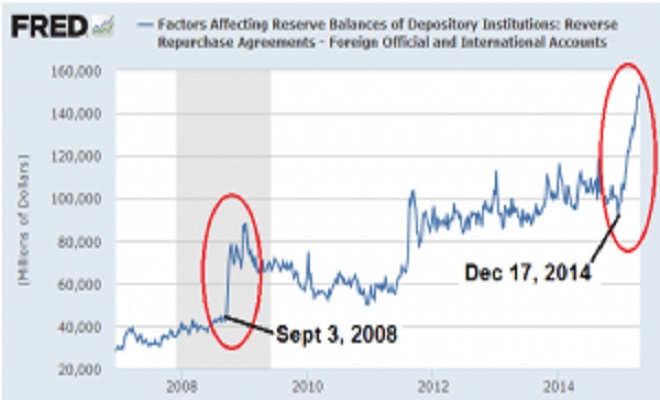

But a good friend and colleague showed me graph this morning that shows my thinking about a derivatives collapse may be correct – click to enlarge:

That graph shows the Fed’s Reverse Repurchase Agreement operations with foreign Central Banks and big foreign banks. A reverse repo is an operation which generally is thought of as being used as a tool to remove short term liquidity from the banking system. However, as you can see from the timing of the first massive spike up, which occurred in early September 2008, it is an absurd notion to think the Fed would have removed liquidity from the system. (Note: the second spike up in 2011 coincided with the Fed’s “Operation Twist” which was essentially a huge QE extension disguised with a “twist” – but nonetheless was done to keep the system from collapsing).

No, instead the massive operation was conducted to INJECT Treasury collateral into the global banking system.Treasuries are used as collateral against derivatives positions. It’s in a sense margin collateral for the big boys. When an entity (typically a bank or hedge fund) takes on a derivatives bet, it needs to post collateral to protect the counterparty from a decline in the value of the bet. Treasuries are the de rigeur collateral, although the ECB now allows everything for collateral except loans to lemonade stands.

When the value of the derivatives bet declines because the value of the underlying asset declines (think: Greek debt, oil debt), more collateral has to posted. Eventually, the market runs out of collateral and there’s a collateral short squeeze. The use of hypothecation exacerbates the situation by several multiples. Please note that Zerohedge intermittently reports big spikes up in Treasury settlement fails. This reflects the extreme shortage of collateral. When collateral has been posted but not hypothecated, it can be called and used for settlement. When that Treasury has been hypothecated by the custodian of the collateral, it becomes harder to call, especially when it’s been hypothecated several times. Big spikes up in settlement fails occur.

Circling back to my postulation that a massive, ongoing derivatives melt-down has started, as the derivatives lose value, more Treasury collateral has to be posted. When the situation becomes extreme, collateral isn’t posted and counterparties begin to fail, especially if the counterparty can’t come up with the cash needed to remedy a derivatives bet gone bad. My bet is that the Greece situation ignited the problem and the collapse in the price of oil threw millions of gallons of napalm on the situation.

The reason I believe this explanation is correct, is from the graph above. We know that in 2008 we were told that a big derivatives accident started in Europe and spread to the U.S. Lehman filed for Chap 11 on Sept 11, 2008. We also know that AIG and Goldman experienced a massive counterparty default collapse in September 2008 that was remedied thanks to rather explicit lies circulated by Ben Bernanke and Henry Paulson about systemic collapse if TARP wasn’t approved.

A reverse repo can be looked at as tool to remove liquidity from the system OR as a tool to inject Treasury collateral into the system. We know the Fed has been “testing” a new Reverse Repo system since mid-2013 that take Treasuries from its “SOMA” holdings (SOMA = the Treasuries the Fed purchased with QE) and use them for reverse repos, including reverse repos with MONEY MARKET FUNDS and foreign central banks/ Too Big To Fail banks. Nothing happens by accident and that spike above shows us why the Fed was “testing” a new reverse repo system.

The only reason the Fed would need to inject massive amounts of Treasuries into the global banking system is because there’s an extreme shortage. A massive derivatives accident requiring massive amounts of collateral to be posted has developed. If Treasuries are not available to post as collateral, while at the same time a massive amount of hypothecated (Treasuries out on loan, several times over) collateral fails are occurring, it will cause the banking system to seize up. The giant spike up shown in the graph above is occurring because the Fed is engaging in an enormous reverse repo operation in order to prevent the global financial system from collapsing.

Remember I suggested some time ago that the elitists like give us a warning before something bad is about to happen. As my colleague John Titus states: “the true elite aristocracy are polite criminals – they consider it gauche to flush the toilet while we’re in the shower without giving us a heads up.”

This is why the IMF issued this warning yesterday for the financial media to publish:

The so-called ‘flash crash’ on US bond markets last October and the collapse of the Swiss currency floor in January showed how quickly liquidity can vanish, acting as “a powerful amplifier of financial stability risks.” LINK: IMF tells regulators to brace for global ‘liquidity shock’

THIS is why stock markets globally are selling off hard today. The S&P 500 is now down over 1%. Typically the Plunge Protection Team has been able to prop it up by noon EST when it falls at the open. So far today the sell-off has accelerated.

I guarantee that the reason for this is unequivocally NOT because the Chinese Government is letting the public short a few more stock issues OR because Bloomberg experienced a widespread terminal outage. But it does go a long way to explaining THIS: LINK

Read More @ Silver Doctors.com

{kind=link}